In an age of electronic payments, the money order is rather old-fashioned. It's been around since at least 1864, and hasn't fundamentally changed since then. A money order is like a check--it's a piece of paper that you give to another person to transfer money to them. Unlike a personal check, which you write yourself, a money order is written by a large institution, such as the U.S. Postal Service, Western Union, or MoneyGram. This is important, because the person you're sending the money to doesn't have to worry about whether you have enough money in your account--they don't have to worry about a check "bouncing" because you don't have enough money to cover it. (But don't let this lull you into a false sense of security--read below about the possible scams.)

How to Buy a Money Order

If you want to send money to someone with a money order, you first get the cash and take it to a place that sells money orders. As we'll see below, there are many easy options such as convenience stores and post offices. You give them the cash and tell them you want to buy a money order. There will be a small fee, usually about $1. So if you are buying something online for $100, and the seller asks for a money order, you go to the store with $101, and they will give you a $100 money order. You will send this to the seller to pay for your purchase.

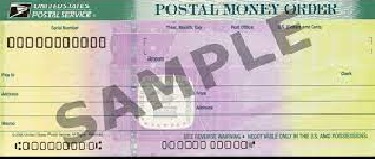

When you get the money order, it will have the amount filled in, but most of it will be blank. It is important to fill out the money order as soon as possible--ideally, before you leave the store. Money orders from the different companies are all a little different, but they will always ask you to write in the name of the person you are sending the money to. Usually, the money order will have the words "Pay To" or "Pay To The Order Of" followed by a blank. On that blank, you write in the name of the person you are sending the money order to.

Most money orders will also have a place for you to write your name and/or your signature. There will also be blanks for your address, the address of the person you are sending it to, or both. There is also usually a box marked "memo," and in this place, you can write in what the money order is for, although this is not required.

The money order contains a receipt. There is a perforated stub, and you tear off this stub before sending the money order. Keep this receipt in a safe place, because if the money order is ever lost or stolen, you can use the receipt to get your money back. You do not send the receipt to the other person--you keep it for your own records.

Where to Buy a Money Order

There are thousands of places where you can buy a money order. Most convenience stores have them, as do supermarkets and big-box retailers such as Walmart. In larger stores and supermarkets, they are usually sold at the customer service counter. At smaller convenience stores, they're sold at the regular counter.

One place that always sells money orders is the U.S. Postal Service. The disadvantage of Postal Money Orders is that the fee is slightly more expensive. For amounts up to $500, the fee is $1.65, and for amounts between $500 and $1000, the fee is $2.20. This compares to Walmart, which advertises that the fee is never more than $1.

But the advantage of a Postal Money Order is first, that it is backed up by the U.S. Government. It's extremely unlikely, but it's possible that the company that issued another kind of money order would go bankrupt, and your money would be lost. One more practical issue, however, is that a Postal Money Order can be cashed at any post office. So if you are sending money to someone who doesn't have a bank account, this is an important thing to keep in mind. You can buy a money order at the post office with a debit card (but not a credit card). In other words, you will need to enter your PIN number as part of the transaction.

Why to Buy a Money Order

Money orders have been around since at least 1864, when the U.S. Post Office came up with them to keep people from stealing money from the mail. Even though they're today only a small part of the financial system, they fill a few important niches.

First of all, there are some people who, for whatever reason, don't have bank accounts. But sometimes these people have bills to pay, and they can't pay them by mailing checks, and they can't pay them online. If they need to pay the rent, or the electric bill, or their car insurance, they could just go to that company's office and pay cash. But this isn't very convenient. It's a lot easier to do it by mail, and money orders allow them to mail their payment. They go to a store or post office and buy a money order for the amount they need to send, and then mail it to the company. The small fee more than makes up for the inconvenience of having to show up at the business in person.

Some online sellers insist on money orders. For whatever reason, they don't want to take online payments. Usually, they are not willing to take personal checks. Unless you show up at their house with cash, the only other alternative is to send them a money order. But beware if an online seller takes only money orders. If there's something wrong with what they're selling, or if they take your money and never send it, there's not much you can do about it if you sent a money order. If you pay online, there's usually a way to get your money back in these situations. So if a seller says that they'll take money orders only, it might be perfectly legitimate, but it might also be a warning sign, so use your common sense.

If you need to send money to a friend or family member, a money order is often a good way to do it. If you're not sure they have a place to cash it, it's best to get a Postal Money Order

from the U.S. Postal Service, because they can cash it at the post office. In fact, if you need to send money to someone in an emergency, you can send it to them General Delivery. They can

pick it up at the post office, and then cash it right there. For more information, see our

blog post about General Delivery.

If you ever engage in large cash transactions, a Money Order can be a good alternative to carrying large amounts of cash. For example, we once sold a trailer to someone living in another state. We met him halfway, and we decided on meeting in a Walmart parking lot. When he arrived, he checked out the trailer and paid us in cash. I didn't want to carry around that much cash, so I went into the store and purchased a Money Order. When I got home, I deposited it into my bank account. If I had been on the road for a long period of time, I could have mailed the money order home, or I could have even deposited it by mail.

If you have a cash business, such as selling items at shows or fairs, a money order can be a safe way of getting your cash home.

How to Cash a Money Order

If someone else sends you a money order, then you have the issue of how to cash it. If you have a bank account, it's usually easiest to deposit it into your own account. Because your bank knows that money orders are good, the money is usually available the next day.

There is, however, one complicating factor about depositing money orders: In most cases, you cannot use remote deposit using your bank's cell phone app. Today, most deposits are done with people's phones. But with a money order, you need to physically take it to the bank to deposit it, or deposit it into an ATM.

If you are not able to deposit the check or cash it at your own bank, there are a number of options. Many (but not all) places that sell money orders also cash money orders, as long as they are the same brand of money order sold by that store. The best example is Walmart. If you need to cash a money order bought at Walmart, then you can cash it at Walmart.

And as mentioned before, you can cash Postal Money Orders at any post office. However, there might be limitations. For example, if you show up first thing in the morning trying to cash a $500 money order, they might not have $500 in the drawer, and you'll need to wait until later in the day.

Wherever you cash a money order, you will need to show proper identification.

How Money Order Companies Make a Profit

You might wonder how companies make any money with money orders. After all, the fee is very small, namely about one dollar. The answer to this question is the "float." When you buy a money order from a company, you give them your cash right away. But it is usually at least a week before the other person receives the money order and cashes or deposits it. In the meantime, the company that issued the money order earns interest on the money.

Why Keep the Receipt

As soon as you buy a money order, you should put the receipt in a safe place, separate from the money order itself. Keep the receipt until you know for sure that the person you sent the money order to has cashed it. If the money order is lost or stolen, you can (eventually) get a refund, but only if you have the receipt.

With some Money Orders, you can also get information by using the receipt. For example, if you have purchased a MoneyGram money order, you can go online to check the status of your money order. With a Postal Money Order, you can fill out a form at the Post Office and request a copy of a previous money order. This can be a valuable tool, because this allows you to get a copy of the recipient's signature on the back of the money order after they cash it.

But the most important reason to keep the receipt is to get a refund if the money order is lost or stolen. This will take some time, but if the money order is never cashed, you will eventually get a full refund. But without the receipt, this will not be possible. So keep the receipt in a safe place, separate from the money order itself.

Watch Out for Money Order Scams!

Money orders have a good reputation, because when you receive a money order, you don't need to worry about the person not having enough money in their account. But just because you have a money order in your hands doesn't mean it is any good. You always have to consider the possibility that it is a forgery!

Money orders all have security features that make them hard to copy. But if you get a money order from a company that you've never seen before, you might not know to look for all of those security features. Unfortunately, computer printers these days can make excellent looking documents. So if someone wants to defraud you, they can print a counterfeit money order at home. So any time you get a money order from a stranger, you need to consider the possibility that the person is trying to cheat you.

If you are selling something online, and a buyer sends you a money order for the purchase price, it's probably legitimate, and you do have some protection. They want you to send the thing they bought, so you do know their address. As a last resort, you can always call the police where they live, and maybe you'll get your money back.

The most common scam is for scammers to send you a money order for more than the purchase price. In other words, you are selling your motorcyle for $500, and they send you a money order for $900. They sound very accommodating, and they tell you they can wait to pick up the motorcycle. They say this because they aren't worried about getting the motorcycle. They just want to steal some of your money.

They will explain that they were given this money order from someone else, and they'll probably have some song and dance about why they can't cash it. They want you to deposit it, and they even tell you that you can wait until it "clears." Then, you can send them their change.

So you get the money order and wait a few days. You might even call the bank, and the bank tells you that the full $900 is now in your account. So you send the person $400. Maybe you mail it to an address they gave you, or maybe they'll ask you to send it by Western Union. After they get the $400, that's the last you'll ever hear from them. If they gave you a mailing address, it wasn't really theirs. They knew your letter was coming, so they waited outside someone's house, and stole it as soon as it was delivered. Or if you sent it by Western Union, then they picked up the money in Nigeria.

A few days or weeks later, the bank calls you and lets you know that the money order was counterfeit, and they're taking the $900 out of your account. Maybe you'll even get in trouble for passing the counterfeit.

Watch out for these scams. If you are selling something, nobody in their right mind will send you more money than you are asking for the item. If they ask for change, it's probably a scam.

About the Author

About the Author

Richard P. Clem is an attorney and continuing legal education (CLE) provider in Minnesota. He has been in private practice in the Twin Cities for 25 years. He has a J.D., cum laude, from Hamline University School of Law in St. Paul and a B.A. in History from the University of Minnesota. His reported cases include: Asociacion Nacional de Pescadores a Pequena Escala o Artesanales de Colombia v. Dow Quimica de Colombia, 988 F.2d 559, rehearing denied, 5 F.3d 530 (5th Cir. 1993), cert. denied, 510 U.S. 1041 (1994); LaMott v. Apple Valley Health Care Center, 465 N.W.2d 585 (Minn. Ct. App. 1991); Abo el Ela v. State, 468 N.W.2d 580 (Minn. Ct. App. 1991).

For more information about attorney Clem, please visit his website, his personal website, or his blog.

Richard P. Clem

PO Box 14957

Minneapolis, MN 55414

Phone: 612-378-7751

e-mail: clem.law@usa.net

Please visit my author page at amazon.com